Per recent reports, as many as one third of applications for business loans get a denial. If you find yourself part of that group, there are some ways to help the situation.

First, try to determine where the problem is.

Possible areas of concern may include:

- Your business profits. Does your business

have a healthy profit margin? Improving your profits by reducing and trimming operational excess and unnecessary business spending can help improve profits. This will boost your chances of approval.

- Your business assets and liabilities. If your balance sheet is out of whack, most lenders will run the other way. If your business is already heavy on debt, then this will be an area of concern you should address.

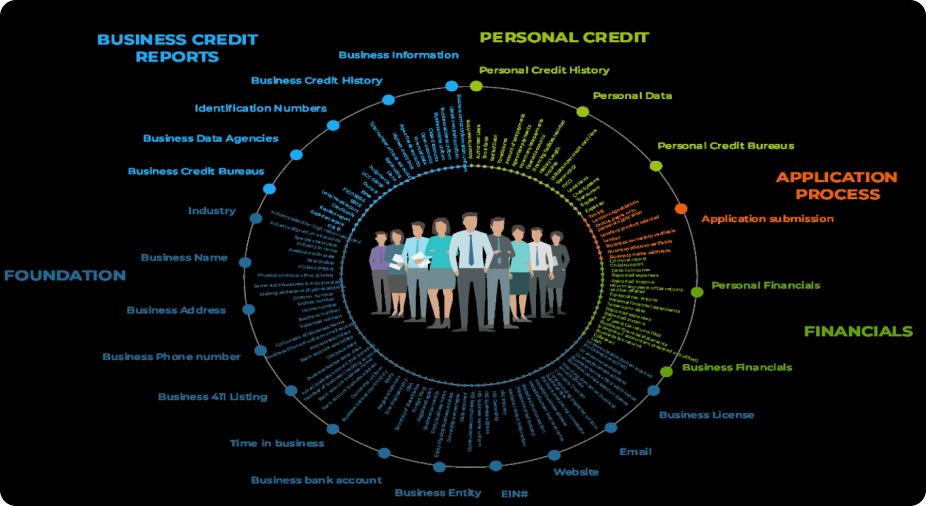

- Your payment histories and business credit profile. How you pay existing obligations will play a role in your approval or denial for credit. If you’ve gotten a business credit denial recently, check your business credit score and other payment performance data.

- Most payment information is only reported for 2 to 3 years (depending on the credit bureau), so if you’ve made a mistake or hit a bump or two in the road, don’t let it worry you. Keep the positive payment history going, and make sure what is being reported is accurate.

- Your bank ratings. If your business bank account balances are often low, this can rule you out for certain types of business credit. Try to maintain

$10,000 or more in your business bank accounts to avoid trouble.

The bottom line is that if you’ve had a credit denial, then there is something about your business making it seem to be a bad risk.

Your job is to analyze and understand your business credit report and business finances. Find where the problem is and take the necessary steps to correct your course.

Sometimes a lack of history or data on your business is a key factor in a credit denial. You can fix this with careful steps to shape your business’s financial picture and credit profile.

About the Author

Mark the President of Commercial Credit Access (“MyCCA”).

Mr. Sheehan spent the last 22+ years working in the equipment finance business helping SMB’s obtain financing to grow their business. He has worked in a variety of positions for banks and independent finance companies. Mark brings a unique wealth of credit and lending knowledge to help his customers improve their business credit and obtain financing.Mr. Sheehan is the driving force behind the release of Commercial Credit Access powered by Fundability (“MyCCA Fundability”). MyCCA Fundability is the leading business cash and credit access system in the world today.